India’s Fintech Revolution: A Glimpse Into the Future of American Finance

This exploration of India’s fintech revolution uncovers the innovations reshaping digital payments, credit, and security—offering a glimpse into how these breakthroughs could influence the future of American finance.

The rise of fintech in India is not just an economic phenomenon—it’s a global case study in digital transformation. Over the last decade, India has built one of the most advanced, inclusive, and fast-moving financial ecosystems in the world.

From UPI (Unified Payments Interface) to digital lending, neobanking, and blockchain innovation, India’s fintech boom is redefining how people save, spend, and invest. The ripple effects of this revolution are beginning to shape the future of finance in America, influencing innovation, regulation, and cross-border collaboration.

Key Takeaways

- India’s fintech growth offers a blueprint for digital-first, inclusive finance.

- UPI and digital identity systems are transforming global payment models.

- The U.S. is adopting lessons from India’s fintech ecosystem for future innovation.

What Is the Fintech Revolution in India?

The rise of fintech in India refers to the explosive growth of financial technology solutions that make banking faster, cheaper, and more inclusive.

India’s fintech ecosystem began to flourish around 2015, driven by three major forces:

- Digital Infrastructure – India’s “Digital Stack,” including Aadhaar (biometric ID) and UPI, enabled instant, paperless transactions.

- Policy Push – Initiatives like Jan Dhan Yojana (financial inclusion scheme) and Digital India accelerated adoption.

- Smartphone Penetration – Affordable data and mobile devices brought digital finance to over a billion people.

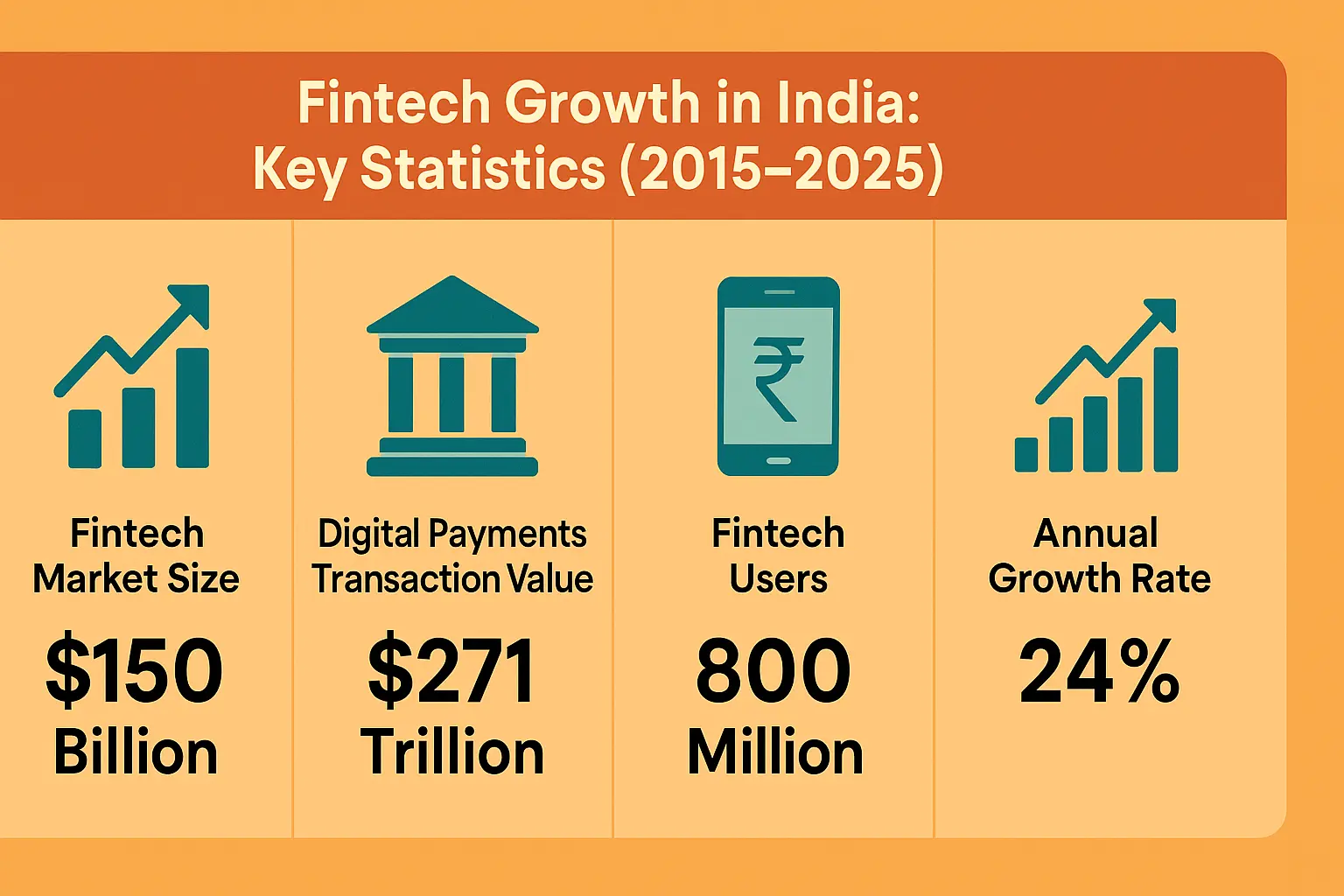

Today, India boasts over 10,000 fintech startups—covering everything from digital payments and insurance to wealth tech and blockchain.

In short, India has created a fintech ecosystem that blends accessibility with innovation, setting a new global benchmark.

$750 Cash App Gift Card

A $750 Cash App gift card may be available to select users. Checking eligibility is quick. You can check if you’re one of them.

Why Does the Rise of Fintech in India Matter Globally?

Because it challenges the old model of how finance works. India’s fintech revolution isn’t just about apps—it’s about rethinking financial infrastructure.

Globally, it has shown that:

- Inclusivity and innovation can coexist. Fintech can serve both billionaires and the unbanked.

- Government-backed open systems can outpace private monopolies (as seen with UPI vs. global payment apps).

- Cross-border inspiration drives faster evolution—America, Europe, and Africa are studying India’s success closely.

The implications are massive. As India exports its fintech architecture and expertise, the world’s financial future is becoming more interconnected, decentralized, and data-driven.

How India’s Fintech Model Is Changing the Game

1. UPI: The Backbone of a Cashless Nation

UPI (Unified Payments Interface) is India’s crown jewel. This real-time payment system allows instant money transfers between bank accounts with zero fees.

In 2025, UPI handles over 12 billion transactions monthly, surpassing even Visa and Mastercard’s domestic volumes. Its open, government-backed model has inspired systems in Singapore, France, and the U.S., where banks are exploring similar interoperable frameworks.

Lesson for America: Open, interoperable, government-facilitated payment rails can drive competition, reduce fees, and accelerate digital trust.

2. Financial Inclusion: Banking the Unbanked

India’s fintech push has brought 500 million+ people into the formal banking system—many of whom never had access before.

Digital KYC, micro-lending, and mobile-first savings tools have turned financial inclusion into an achievable reality.

Lesson for America: Fintech can bridge inequality gaps if built on inclusion, not just innovation.

3. The Rise of Neobanks and Digital Lending

Indian startups like Razorpay, Jupiter, and Niyo are pioneering neobanking, providing app-based accounts without traditional branches.

Similarly, digital lending platforms use AI and alternative data (like phone usage) to assess creditworthiness—opening access for small businesses and gig workers.

Lesson for America: Decentralized lending models can serve the underbanked and accelerate economic participation.

4. Regulatory Innovation: India’s Secret Advantage

India’s regulators—especially the Reserve Bank of India (RBI)—have walked a fine line between enabling innovation and enforcing stability.

By introducing frameworks for digital KYC, account aggregation, and open banking, India has achieved what many Western nations still debate.

Lesson for America: Regulatory flexibility, paired with digital public infrastructure, drives safe innovation.

Can America Replicate India’s Fintech Success?

That’s the billion-dollar question. While the U.S. leads in venture capital and advanced financial products, it still faces challenges in interoperability, inclusion, and affordability.

India’s fintech model thrives because it’s publicly built but privately scaled—a synergy between policy and innovation. In contrast, the U.S. system is privately built and fragmented, limiting universal access.

However, the rise of FedNow, America’s new real-time payment system, hints at a shift toward India’s open architecture model.

In short: The U.S. can learn from India’s fintech playbook—but must adapt it to its own socio-economic and regulatory environment.

How India’s Fintech Is Influencing Global Finance

1. Cross-Border Payment Integration

UPI partnerships with Singapore’s PayNow and discussions with the UAE and UK mark the start of a global payment web.

This interoperability could redefine remittances—especially for the $100 billion India receives annually from overseas.

Impact on America: Faster, cheaper, transparent cross-border transfers could reshape U.S.–India trade and remittance flows.

2. The Global Rise of Digital Public Infrastructure (DPI)

The World Bank and IMF have hailed India’s Digital Public Infrastructure as a model for inclusive growth. DPI—a stack of interoperable, open technologies—could form the backbone of future global finance systems.

America, historically reliant on private networks, is now exploring similar public-private ecosystems.

3. Fintech Exports and Talent Flow

Indian fintech companies are expanding globally—Pine Labs, Paytm, and Razorpay are entering Western markets.

Meanwhile, Indian fintech professionals are helping shape policies and innovations in U.S. institutions and startups.

The result? A knowledge transfer loop accelerating financial modernization on both sides.

Best Practices America Can Learn from India’s Fintech Boom

- Build Digital Infrastructure First: Focus on scalable, interoperable systems—like UPI and Aadhaar.

- Encourage Open Ecosystems: Avoid monopolies; promote competition through public APIs.

- Foster Regulatory Sandboxes: Allow innovation within safe, supervised environments.

- Invest in Inclusion: Ensure fintech serves the underserved, not just the affluent.

- Leverage Data Responsibly: Use AI and analytics ethically to expand credit access.

Common Myths About India’s Fintech Growth

Myth 1: India’s fintech success is government-run.

Reality: The government built the rails; private startups built the services.

Myth 2: UPI only works for small payments.

Reality: UPI handles everything from micro-transactions to corporate payrolls.

Myth 3: America is already ahead.

Reality: The U.S. leads in innovation but lags in inclusion and real-time infrastructure.

Expert Views and Global Reports

- IMF (2024): “India’s fintech model has demonstrated how public digital infrastructure can accelerate inclusive growth at scale.”

- World Bank (2025): “UPI and Aadhaar stand as global exemplars for digital finance frameworks.”

- McKinsey (2025): “If replicated, India’s fintech framework could add $500B to the U.S. economy through efficiency gains and inclusion.”

- Industry Leaders: American fintech CEOs increasingly cite India as the world’s “fintech lab.”

$500 Walmart Gift Card

A $500 Walmart gift card may be available to select users. Checking eligibility is quick. You can check if you’re one of them.

FAQs

1. What drives the rise of fintech in India?

Digital infrastructure, supportive regulation, and mass smartphone access have powered India’s fintech boom.

2. How does the rise of fintech in India impact the U.S.?

It offers lessons in interoperability, inclusion, and low-cost payments—elements that can modernize American finance.

3. Can the U.S. adopt systems like UPI?

Yes. With FedNow and open banking initiatives, the U.S. is moving toward similar interoperable payment systems.

4. What role does India play in shaping global finance?

India’s fintech ecosystem is influencing cross-border payments, financial inclusion models, and digital policy frameworks worldwide.

5. Why is India’s fintech model unique?

It blends public infrastructure with private innovation, creating an ecosystem that’s scalable, inclusive, and globally replicable.

Key Takeaways

- The rise of fintech in India has become a global benchmark for inclusive, scalable finance.

- India’s UPI system and digital identity stack are shaping how nations approach digital payments.

- America can learn from India’s model to improve interoperability, inclusion, and innovation.

- The future of global finance lies in collaboration between public infrastructure and private innovation.

- India’s fintech revolution is not just changing its own economy—it’s reshaping the world’s financial future.

Conclusion

The rise of fintech in India marks a defining chapter in global finance. It proves that innovation and inclusion can move together when technology, policy, and entrepreneurship align.

For America, India’s fintech journey isn’t just a success story—it’s a blueprint for reimagining finance in the digital age.

If the U.S. embraces openness, interoperability, and inclusion as India has, the future of finance could be faster, fairer, and more connected than ever before.